Whether you’re buying your first franchise, expanding an existing business, or launching a new venture, securing financing is often one of the biggest challenges. Similar to an SBA loan in the United States, the Canada Small Business Financing Program (CSBFP) is designed to make that process easier by helping eligible small businesses qualify for financing through participating lenders. In this guide, we’ll explain how the program works, who qualifies, what expenses are eligible, and how a CSBFP loan can help finance your business.

What Is the Canada Small Business Financing Program (CSBFP)?

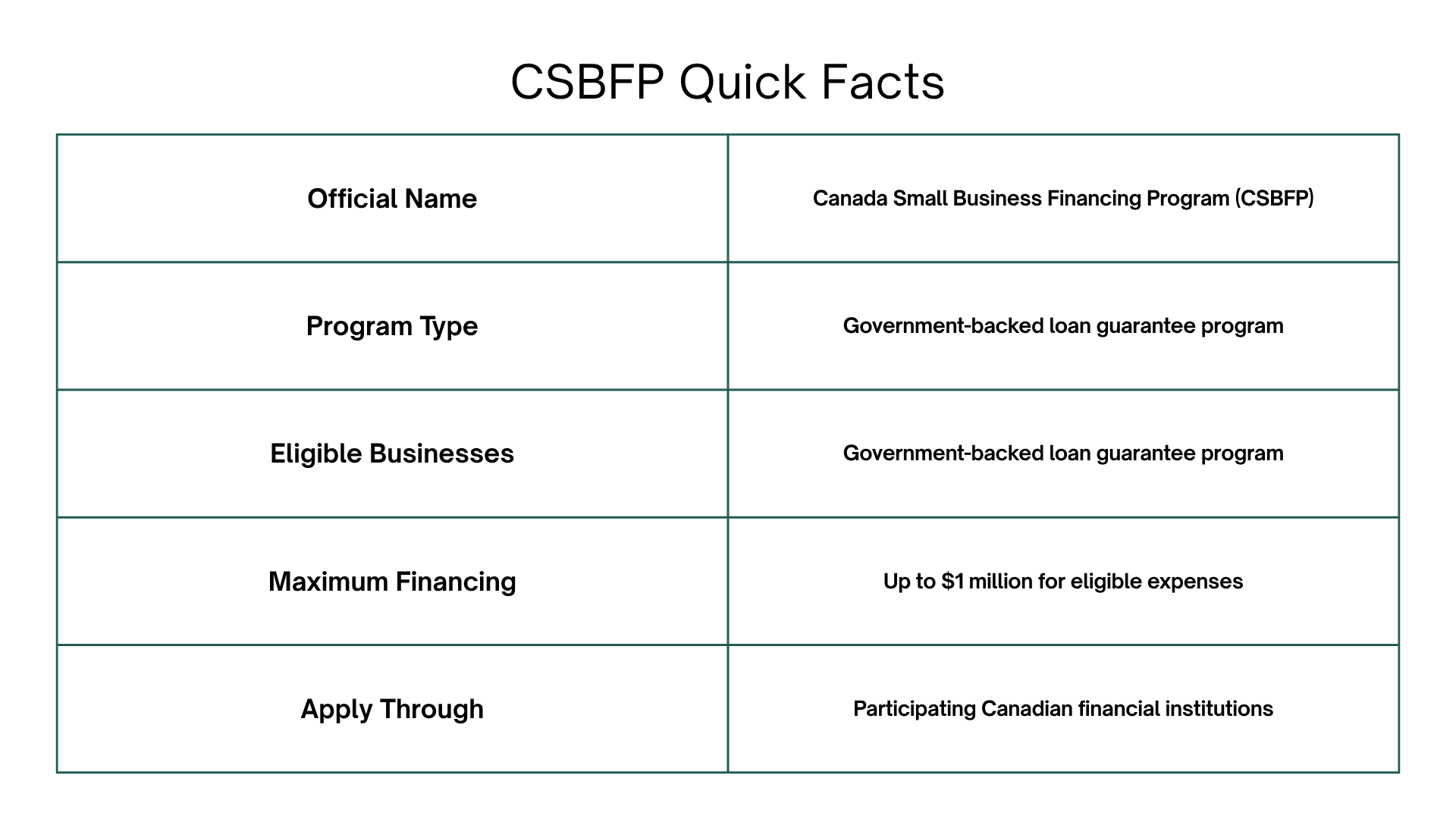

The Canada Small Business Financing Program (CSBFP) is a loan guarantee program that helps small businesses obtain financing through participating financial institutions. The government guarantees a portion of eligible loans, reducing the lender’s risk and making it easier for entrepreneurs to finance expenses such as equipment, leasehold improvements, commercial real estate, and more.

Understanding the Different Acronyms

If you’ve been researching small business financing in Canada, you’ve probably come across several different acronyms that appear to describe the same program. While they’re closely related, they don’t all mean the same thing.

- CSBFP (Canada Small Business Financing Program): The official name of the Government of Canada’s loan guarantee program for eligible small businesses.

- CSBF: A commonly used abbreviation for the Canada Small Business Financing Program. Although not the official acronym, it’s frequently used in articles, discussions, and online searches.

- CSBFA (Canada Small Business Financing Act): The federal legislation that establishes and governs the Canada Small Business Financing Program.

- CSBFL (Canada Small Business Financing Loan): A term commonly used to describe a loan issued under the Canada Small Business Financing Program.

In short, these acronyms all refer to the same government-backed financing initiative or the legislation that supports it.

7 Key Features of the CSBF Program

It’s important to understand the terms and conditions of the CSBF to evaluate if it’s a viable option for you to purchase a franchise.

1 – Interest Rates

Both floating and fixed interest rates are available to the borrower. These rates will vary depending on which financial institution is providing the loan. However, the maximum chargeable for a floating rate is the lender’s prime lending rate plus 3%. For a variable rate, it’s the lender’s single-family residential mortgage rate for the term of the loan plus 3%.

2 – Term Loans

The program offers term loans to finance the purchase or improvement of assets. A term loan “provides borrowers with a lump sum of cash upfront in exchange for specific borrowing terms”. Borrowers often prefer term loans since they “offer more flexibility and lower interest rates” (Investopedia).

3 – Eligibility

Businesses eligible for the CSBF have gross annual revenues of $10 million or less. Farming businesses are not eligible for this program. Interestingly, charitable, religious, non-profit organizations (NPOs) used to be excluded from this program. However, since June 30, 2021, they are included provided that they carry on a small business.

4 – Loan Amounts

The maximum loan amount is $1 million. As of July 4, 2022, the CSBF also offers a line of credit. This can exceed the loan amount but is capped at $150,000.

5 – Flexible Use

In short, the CSBF term loan can be used for:

- Purchasing or improving commercial real estate

- Leasehold improvements, such as renovating a leased office, retail, or commercial space

- Purchasing or upgrading equipment, machinery, or other eligible business assets

- Financing eligible intangible assets, such as software or intellectual property

- Covering certain working capital costs associated with eligible assets

- Paying the program’s registration fee

While there are several options for how to use the CSBF loan, there are a few limitations. In general, a CSBFP loan cannot be used for:

- Paying off existing business or personal debt

- Purchasing goodwill associated with a business acquisition

- Buying shares or ownership interests in a company

- Covering personal or household expenses

- Financing operating expenses that aren’t eligible under the program

Check out Canada Small Business Financing Program Guidelines for more specific information regarding the term loan stipulations.

6 – Government Guarantee

As mentioned already, this program makes it so that the Canadian government shares the risk of the loan with the lenders. If the borrower defaults, then the government will cover 85% of the losses. This guarantee makes it easier for small businesses to obtain a loan from participating financial institutions.

7 – Loan Repayment

While the specific terms for repayment will depend on each loan, the maximum term is 15 years. The loan can be amortized for a longer period, but after 15 years the remaining balance will be converted to a conventional loan. While at least one payment of principal and interest must be scheduled annually, the schedule for the rest of the payments can be flexible.

The maximum term for the CSBF’s line of credit is 5 years with options for renewal before the end of the term.

What is the Application Process?

You can apply for the CSBF if you meet the definition of a small business and are not in the agricultural industry.

Steps to Apply

If you’re interested in applying for the program, you can take the following steps:

- Find a financial institution eligible for this loan (check out this map for a list of lenders)

- Present a business proposal that outlines the size of loan you’re looking for, how it will be used, and your plan for repaying the loan

- If the loan is approved, then you will negotiate the interest rate and term of the loan with your lender

- If your loan application is rejected, apply with another financial institution that has different lending criteria

As you take the steps to apply for this program, remember that having a solid business plan can increase the lender’s confidence in giving you a loan.

Required Documentation and Paperwork

Let’s say the lender approves the loan application. Now, in order to obtain a CSBF loan, both parties will need to sign a document with a plan that includes the following information:

- Loan amount

- Interest rate

- Repayment terms

- Payment frequency

- Due date for the first payment

Regarding the CSBF line of credit, both parties must:

- Sign a document before opening the line of credit

- Specify the terms (amount, interest rate, credit terms)

- This can be any document used to secure repayment of a line of credit (promissory note, loan agreement, bank contract, etc.)

Who Is the Canada Small Business Financing Program Best For?

The CSBF is designed to help entrepreneurs who may not otherwise qualify for traditional business financing. It can be a valuable option for a variety of businesses, including:

- First-time entrepreneurs looking to start their first business or purchase a franchise.

- Franchise buyers who need financing for eligible startup costs such as equipment, leasehold improvements, or commercial property.

- Existing small businesses planning to expand, relocate, or renovate their operations.

- Businesses purchasing equipment needed to launch or grow their company.

- Companies improving commercial space through leasehold improvements or renovations.

Ready to Finance Your Franchise in Canada?

If you are looking to buy a franchise, then you should definitely explore the CSBF program as a viable financing option. You should also reach out to FranNet for help navigating the process. Our expert franchise consultants will not only help you evaluate your funding options, but they will match you with the right franchise. You won’t have to pay a dime for our services. You have nothing to lose and everything to gain. Schedule your free consultation today!